The protest movement by truckers in Canada against pandemic-linked restrictions has raised money – nearly a million dollars – via bitcoin. This is after fundraising platforms backed out and the government began freezing bank accounts linked to the movement.

“20% of funds raised are being consolidated in a hardware wallet for the truckers organizers to use for immediate needs including food, hotel rooms, legal aid and fuel… 80% of funds raised are being consolidated into a multisig wallet.”

The keyholders’ identities are not being made public, ostensibly to prevent authorities from coercing them to give up access.

A sister article on the same site used the phrase “permissionless financial rail” to describe this use of bitcoin.

This is quite accurate – the ‘rail’, or mechanism has worked in spite of permission being denied.

This isn’t bitcoin’s first use as “permissionless financial rail”: in 2020, Nigerian protest against a special-powers law were funded using decentralised tokens when bank transactions were allegedly “being slowed down”:

“How bitcoin powered the largest Nigerian protests in a generation”, Quartz.

Finally, remittances in bitcoin and other cryptocurrency tokens are a post in itself – they are a permissionless alternative to remittance incumbents – including banks – that charge super-high fees for cross-border money movement.

The common thread: what we are seeing is a revolution in the freedom to transact.

Something so fundamental we barely pay attention to it in real life – until that freedom is taken away. We assume we can always accept money from someone who is willing to send it to us. We assume we can use any app, any service by paying for it.

Decentralised networks of value ensure that that freedom can never be taken away.

But that freedom to transact applies to everyone. Both “good” Nigerian anti-special-powers protestors and “bad” Canadian anti-vax truckers.

With that playing field levelled, it truly becomes a battle of ideas – when all parties have unrestrictable access to capital, the “winner” is the one who can use that capital to make their case more effectively.

I am fascinated by the implications of this for the society of tomorrow.

When regulation is implemented, “Does it mean that Indian tax residents will not be allowed to hold tokens at all in non-custodial wallets?” asked Rahul Gaitonde… “And does that hold true today as well? So, if you were to have an account at an Indian exchange and you were to send the money to a non-custodial wallet, is that a violation?”

One of the more interesting applications of NFTs is in games.

The well known game Cryptokitties from 2017 is one of the earliest examples – you can breed unique ‘cats’ that inherit combinations of twelve specific traits that made some combinations rare, and those kitty NFTs valuable.

(Fun fact: The transfer and breeding of the kitties ended up creating bandwidth issues on the Ethereum blockchain, crowding out other transactions and sending ‘gas’ or transfer fees through the roof, giving rise to a whole new set of projects to scale the Ethereum blockchain, probably the most famous of which is Polygon)

In-game NFTs have exploded since, with developers representing all kinds of things on the blockchain and players creating, buying, trading – and playing with them. Axie Infinity took a Cryptokitties-like game concept to another level, with ‘battles’ between Axies, or NFT characters, in return for rewards. Axie got public attention in a 2021 documentary describing how some people in the Philippines who lost their jobs in the pandemic took to playing Axie Infinity to earn tokens & exchange them for ‘real’ money.

Decentralised gaming is dizzyingly broad and varied, and impossible to do justice to in a single post. But here are some of the more well known ones: Decentraland is a trading-oriented game around unique parcels of land in a virtual universe, Upland does the same thing but maps real-world locations into its virtual world. Sandbox is a similar game where one can generate a seemingly infinite universe composed of NFT land parcels and features by using resources like sand, water, soil, lightning and others. My Neighbour Alice does the same thing but for neighbourhoods and adds a strong social element. Star Atlas takes the same dynamics to space exploration. Mist and Ember Sword are action/combat-oriented role playing games with in-game collectibles that you can win, earn, and trade on NFTmarketplaces like Opensea. There are even more games that have NFTs as core elements in the gambling, racing, puzzle, business simulation and several other genres.

What Decentraland looks like

That has given rise to platforms and marketplaces. We just linked to OpenSea, which is a general-purpose NFT marketplace for assets on Ethereum, which also hosts gaming NFTs. Entities like Yield Guild Games buy, sell and rent out Axies, and now all sorts of other in-game NFT assets like virtual land. YGG is an example of decentralised finance intersecting with decentralised gaming. Enjin is a project whose software (or SDK) game developers can user to create, provision, issue, store, trade and destroy in-game virtual goods, whether they’re currencies or NFTs. Xaya is another similar project. Mobox helps create DeFi products with game elements, such as liquidity pools and yield farming, opening up revenue opportunities for game token holders.

There’s the matter of how the object renders across different games, how its utility translates between different games, its constraints, the fact that they be on different chains and use different standards even on the same chain, and so on. To that end, Cryptomotors is a “professional car design studio… creating decentralized digital vehicles powered by the Ethereum blockchain.” And, as an owner of one of these tokens, you’ll be “able to use your crypto vehicles in different 2D, 3D, and VR games and platforms”.

One of the central elements of issuing virtual goods – a concept which is decades old – as blockchain assets is to enable, in principle, users to truly own those goods. For example, a player who owns an element that’s an Ethereum-standards-compliant NFT can store it in a wallet whose private keys only they own. They can sell it on marketplaces like Opensea, rent it like Yield Guild Games does. And, as an increasing number of games are enabling, use the same element across multiple games (subject to questions about IP).

The big difference here is that none of the wallets, marketplaces, rental services or others are built by the game developer. They exist independently of the game developer, and aren’t even limited to games. A single wallet could hold Ethereum currency itself, NFT art, membership token NFTs, vaccination cards issued as NFTs, and in-game elements. That creates a true ecosystem around in-game elements, which – in principle – live on a blockchain forever and – given the right design – can well outlive the original game developer.

Some games have taken community engagement further by handing over part of direction setting and decision making to holders of their community, or governance, token – turning themselves into a decentralised autonomous organisation or DAO. Decentraland, for instance, states that “you, the users… are in control of the policies created to determine how the world behaves… upgrading LAND and Estates to add more features and protocol upgrades, specifics and dates of future LAND auctions… addition of new wearables to the Decentraland World, Builder and Marketplace, replacing members of the Security Council”.

This is a whole new way of thinking about and designing games and building community.

Correspondingly, the interest in the native tokens of several of these projects has caused their dollar prices to skyrocket: Axie’s token AXS is up over 17000% since the beginning of 2021, Sandbox’s native token SAND nearly 14000%, Decentraland’s nearly 4000%, Enijn’s nearly 1700%.

However. Among the more well established game studios, it’s not clear how well they get the idea of tokenised in-game elements. Ubisoft, the company behind games like Assassin’s Creed, Far Cry and the Tom Clancy’s… series, announced its foray into in-game NFTs earlier this month, with items like guns, helmet and face masks for one of its combat games.

It wasn’t well received because the design of its ‘Quartz’ programme seem to negate the whole point of decentralisation. The tech publication Ars Technica is quite blunt, starting with the title of its coverage: “Ubisoft’s first NFT plans make no sense”.

For a supposedly decentralized and “open” technology, Ubisoft places a lot of restrictions on who can own and use Digits. Quartz users have to be 18 years old, reside in one of a handful of countries… and use two-factor authentication on their Ubisoft Connect accounts.

Quartz owners also have to reach “XP Level 5” in Ghost Recon Breakpoint before they can collect or use the NFTs… That XP level status is confirmed by linking Quartz to your Ubisoft account, which is, of course, centrally controlled and subject to its own terms of use above and beyond the detailed Quartz terms of use.

Players who don’t meet any of Ubisoft’s requirements “will not be able to acquire Digits whether on the Ubisoft Quartz platform or an authorized third-party marketplace, nor have another player transfer their Digits to you…

Digits are what Ubisoft calls its in game items. And finally, speaking of these Digits themselves,

A single player, for instance, can only have one copy of each distinct Digit edition… “Owning” that NFT doesn’t give you the right to create derivative works, to use the item in videos, to sell merchandise that includes the item in it, or even to sell “fractionalized interests” in the associated NFT…

But at the same time

Ubisoft says it doesn’t have the ability “to reverse or cancel transactions.” So if you get scammed out of your item somehow, the company can’t help you.

If players don’t own them, can’t port them, can’t sell them except in some cases, and can’t use them in any context other than as defined by Ubisoft, why are they even NFTs? The long-running game-focused website Kotaku picked some comments from those on Ubisoft’s YouTube announcement video, one of which was

Ubisoft, once again, giving us something we didn’t ask for, don’t want and won’t enjoy.

Reactions from other game developers have been varied. The game developer Valve, maker of Counter Strike, Half Life, Team Fortress and others, has already stated that it wasn’t going to allow any NFT items or crypto related content on Steam, its game platform and store. EPIC games, Atari and SEGA have all indicated different levels of interest in the space.

Finally, in some cases developers have also had to contend with resistance from their player community. Like Ubisoft, another game developer announced plans for an in-game NFT element in the game Stalker 2: Heart of Chernobyl. Specifically, it would “auction off the chance for one player to have their face photogrammetrically scanned onto a non-player character (NPC), in what the studio calls the “the first-ever metahuman.””. It’s unclear to me how that would translate to an NFT, or whether the studio even understood the idea or ethos of decentralised elements in a game, but in any case, the outcry on social media from their user base was loud enough that it cancelled those plans.

In conclusion we’re just seeing the bare beginnings of interoperable, user-owned, programmable in-game elements represented as NFTs. We’re only seeing the beginning of how they interact with the other trends in the evolution of the decentralised ledger space, including DeFi and DAOs, and with other tech innovations like Facebook’s virtual reality based pivot to what it’s calling the Metaverse. Even as someone who isn’t an avid gamer, I’m rather curious about innovation that’s to come in this space and how it influences and is influenced by innovation in other areas of the decentralised universe.

(1) “The impact of a crypto payments ban on the NFT, blockchain and DeFi space since transaction fees need to be paid in crypto.”

Gaitonde, the crypto investor and company advisor, said that the rules as outlined in the draft bill will allow people to buy and sell tokens but potentially exclude Indian investors from participating in the broader decentralized ledger technology ecosystem.

“If crypto regulations state that only licensed crypto exchanges can hold tokens, the universe of crypto projects available to people shrinks greatly because it is impractical for any such exchange to list tokens from every decentralized project,” Gaitonde said.

“Similarly, if regulations forbid the use of non-custodial wallets, then DeFi projects, NFT marketplaces, decentralized software or dApps, blockchain-based games and such innovations become inaccessible,” he added. This is because the decentralized world largely supports such wallets — which are used to swap NFTs and other artifacts with crypto tokens.

(2) “Do you think [the proposed punitive measures are] more stringent than what the crypto community was expecting given that violations will be treated as a cognizable crime alongside murder, theft and kidnapping? “

… [a]ccording to Rahul Gaitonde, a crypto investor and adviser to blockchain companies, the harsh ban on crypto should not come as a surprise since an earlier crypto ban bill draft from 2019 also recommended treating infractions as cognizable offenses. The “Banning of Cryptocurrency & Regulation of Official Digital Currency Bill, 2019” draft reportedly forms the backbone of the current bill.

However, Gaitonde is still hopeful the final bill will allow more flexibility with cryptocurrencies since the government has held multiple consultations with industry experts and has expressed an interest in preserving innovation.

I was a guest on a podcast recently for a long and pretty rewarding conversation about decentralisation of trust, what it means for a crypto project’s decentralised token to capture value, speculation vs intrinsic value, what due diligence/fundamental analysis of decentralized projects could look like, ‘investing’ in tokens, and regulation.

It’s about an hour and five minutes long – no ads.

The host of the podcast thought – last month– that an episode talking about first principles of decentralised ledger technology (DLT) might be a good idea given the rumours and consequent panic then around regulation of the DLT space in India.

On the podcast show notes page, I have also added what newsletters, podcasts and websites about the subject I personally read/listen to.

In June this year, El Salvador in Central America became the first country to make cryptocurrency, specifically bitcoin, legal tender. Earlier this week, businesses around the country actually began accepting bitcoin for payments, including salaries.

The background

The current thirty nine year old president of El Salvador has long championed the idea of cryptocurrency as legal tender. He first discussed it publicly as mayor of the capital city of San Salvador.

This was Bukele’s Twitter profile image a while ago. For real.

His take is that it could provide “an accessible financial platform for Salvadorans who don’t have a bank account, about 70 percent of the population.”

He and other proponents have also pointed out that USD six billion, or over twenty percent of the country’s GDP comes from remittance by citizens who live overseas, and that cryptocurrency had the potential to signficantly reduce fees for sending money into the country.

Interestingly, an anonymous donor had kicked off a pilot for the last couple of years in the village of El Zonte, which earned the nickname Bitcoin Beach. The results had been mixed – some people “didn’t have higher-end cellphones needed to download the app, while others said they had doubts about how it worked.”

Importantly, bitcoin transactions in the village take place using an app named Strike, which has now also been involved in the national rollout of bitcoin acceptance. Strike, developed by the US based company Zap, processes transfers over the Lightning network that runs on top of the Bitcoin blockchain, as opposed to making actual on-blockchain Bitcoin transfers.

New Option using Bitcoin – son uses the new Strike App (https://strike.zaphq.io/) linked to his US bank account to send $100 in BTC over Lightning network. Cost to son $0 and 3 minutes of his time. Cost to mom $0 and receives payment immediately, directly to her phone.

She can buy milk from the local store that accepts Bitcoin (even sending payment directly from her phone sitting in her house and having someone deliver.) She can also pay her electric bill without leaving home, or walk down the street and eat at the local restaurant.

The $7 fee and $2 bus fare mean the transaction costs using Western Union would be 9%, and more importantly a big waste of time and effort. Bitcoin over the Lightning Network fixes this.

From the Bitcoin Beach website

The Lightning network

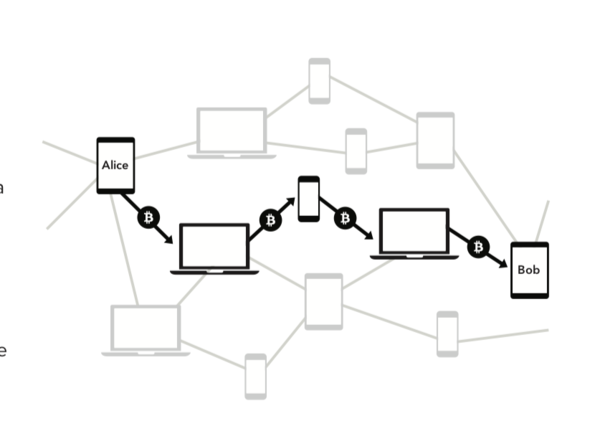

Strike and Chivo, the ‘official’ Bitcoin wallet app at the national level, are both Lightning network apps. Lightning is a ‘Level Two’ technology, which means it works on ‘top of’ the bitcoin blockchain, not on it. It makes a simple tradeoff: it increases speed of transfer for greatly reduced fees. It does this at the expense of decentralisation.

The Lightning network has its own nodes, separate from bitcoin, but connected to it. Two parties on the Lightning network create a private ledger between themselves, called a channel. They can send several transactions back and forth rapidly and cheaply between themselves, no Bitcoin blockchain involved. When they close the channel, the net result is written to the Bitcoin blockchain, with its associated speed and fees and finality.

For several million transactions daily between several million citizens, as you’d expect even in a small country like El Salvador, the Bitcoin blockchain isn’t going to cut it. The Bitcoin network today processes about seven or eight transactions per second at its maximum throughput. Layers like Lightning are a practical necessity for everyday payments. Bonus, they also make micropayments of fractions of a cent possible.

People also protested the overhead of having every store, every vendor, every roadside operator being forced to accept bitcoin (it being legal currency now!). And not everyone is happy with the president’s declaration in June that “people investing three Bitcoins in country’s economy will be given citizenship by the government.”

But. Despite all of this. Bitcoin is now, alongside the US Dollar, the official currency of El Salvador.

In conclusion

This is a big deal – as a few people have pointed out, a nation-state has adopted as its currency a twelve year old technology that runs only on computers, mostly outside of its borders, owned by everyone and no one.

The promise of low remittance fees is very real. So far it’s been impractical not because of technology but because in most country there are no easy or legal ways to convert received cryptocurrency into fiat currency. That’s no longer the case in El Salvador.

And finally, it’s also true that the vast majority of the El Salvadorian population has been failed by its banks and financial system.

As we’ve seen many times on this newsletter, decentralised finance is remaking large parts of the traditional finance space: storing money, payments, lending and borrowing of all sorts, investments, insurance, and many others, offering conveniences that are not even possible without decentralisation.

There’s no expectation that this move will magically solve the country’s financial inclusion problems, but it does open the door to Defi entrepreneurs to bring their services to the ordinary El Salvadorian.

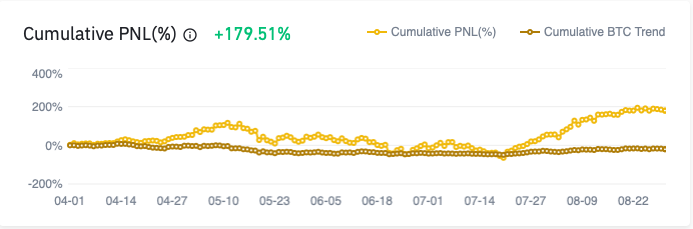

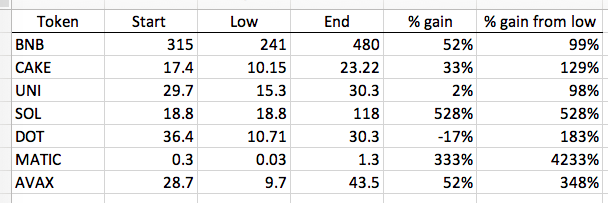

My holdings in Binance were up nearly 180% – or nearly 2.8x – in the five month period 1st Apr 2021 to 31st August 2021.

During this time, Bitcoin was down nearly 20%, from USD 59,000 to USD 47,300. Ethereum was up a little under 70%, from ~USD 1950 to ~USD 3300.

So the holdings did quite a lot better than either of these two coins by themselves.

Here is a quick peek into what I do.

Dollar-cost-averaging

In other words, making regular token purchases.

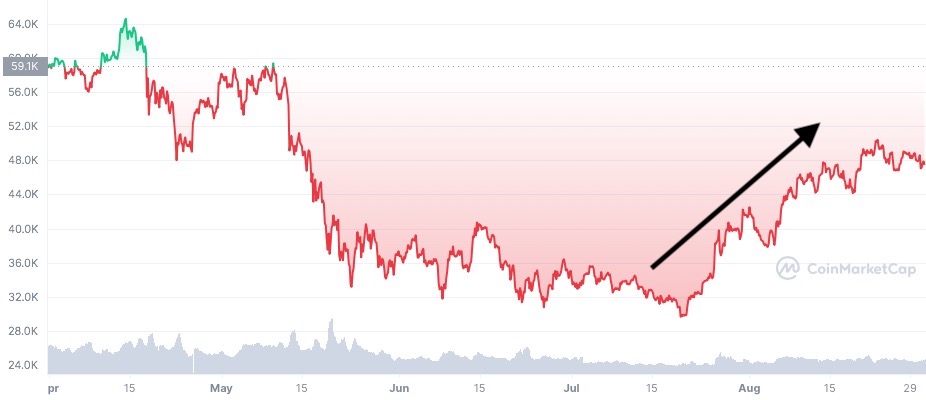

Bitcoin went down from USD 59,000 to nearly USD 29,000 before climbing to USD 47,000. Some of my holdings rode that rise.

Similarly, Ethereum rose to nearly USD 4,300, plummeting to almost USD 1,700 before rising back up to USD 3,300. Some of my holdings benefited from that last steep climb.

Bitcoin (left) and Ethereum from Apr to Aug

Diversification

I hold a number of alt coins in addition to Bitcoin and Ethereum. These are all tokens whose projects I see merit in. Some of them are Binance Coin (BNB), Pancakeswap (CAKE), Uniswap (UNI), Solana (SOL), Polygon (MATIC), Avalance (AVAX).

I also added these in more than one tranche during this period. Here is how they have done over the five month stretch, and from their low during this time. As you can see, some of them have done rather well:

Start is 1st Apr; End is 31st Aug

I also hold others in small proportions, whose rise and fall doesn’t affect the overall performance much. (and I hold some stablecoins whose value, by definition, doesn’t change).

Yield farming and staking

Through staking and adding to liquidity pools. Explore the Earn section on the Binance exchange for these products. I also participate in these on the decentralised exchange Pancakeswap, which has a wider range of staking pools and liquidity pools than Binance itself. There are further layers of optimisation above this to take advantage of, which I may describe in a separate post.

Several of these offer attractive yields:

But – and I cannot emphasise this enough – there is risk proportional to that return. For instance in liquidity pools, you should at least be aware of the concept of impermanent loss.

I mitigate these risks with some pretty basic principles:

One, I only stake or add to pools with tokens that I am comfortable holding, whose use in the parent project I’m familiar with. I do not swap to acquire tokens only for the sake of attractive yields.

Two, I plan to hold these tokens for the long term. As of this writing, indefinitely (or until the project no longer shows promise). That protects me a great deal against impermanent loss, because I’m less likely to remove liquidity and realise those losses, if any.

So there you have it

Dollar-cost-average into tokens, especially because they are so volatile

Diversify your holdings, into projects that you understand and believe in

Put those holdings to work through yield farming and staking, as long as you understand the risks involved.

Not all months, quarters or even years will be like this. Most of the crypto space is still largely speculative, so even dollar-cost averaging into good tokens that work hard for yields may result in nought as the market itself crashes. During those times it’s useful to be clear about why you want to hold crypto in the first place.

PS: what I describe is the active part of my holdings. I also hold Ethereum and Bitcoin in non-custodial wallets outside of Binance. Those are out-of-sight, out-of-mind holdings (“hodlings”). I keep the wallet passphrases secure but don’t check the value in those wallets very often.

Finally: consider subscribing to my once-a-week crypto newsletter for more like this.

What if hydroelectric power projects in India could do the same?The state I live in, Maharashtra, has one of India’s largest hydroelectric power plants, Koyna.

Now, the Maharashtra State power generation utility lost ₹230 crore or ~$30 million in 2019-20. The price of bitcoin today is roughly $45,000. That means it would take about 30 million / 45,000 = 666 bitcoin at these prices to make up for the shortfall.

How much power would that take?

A few months ago, CNet estimated that it took about 1544kWh to mine one bitcoin. At that rate, to mine 666 bitcoin it would take 1544kWh x 666 = ~1030MWh.

So very roughly, that’s 100% of Koyna’s output for 31 minutes, or 1% for 300 minutes, or 0.001% for 300,000 minutes or 83 hours. One would think that the power plant could spare that much extra capacity over the course of a year.

Obviously this is capped by the bitcoin mining rate (today ~6 ¼ bitcoin is mined as reward every 10 mins). And competition from miners throughout the world. But over a *year* it should be doable.

This is a simple thought experiment. The number are rough, but in the right ballpark. The market value of a marginal MWh of generated power is now measurable. The question is whether utilities in India and globally will take act on it.

An inter-ministerial panel has recommended that “all private cryptocurrencies, except any virtual currencies issued by state, will (sic) be prohibited in India”, the Economic Times reported a couple of weeks ago.

The terminology caught my eye.

We’re used to thinking in binary terms: owned by the government (ostensibly in public trust) or owned by a private corporation (but regulated by the government):

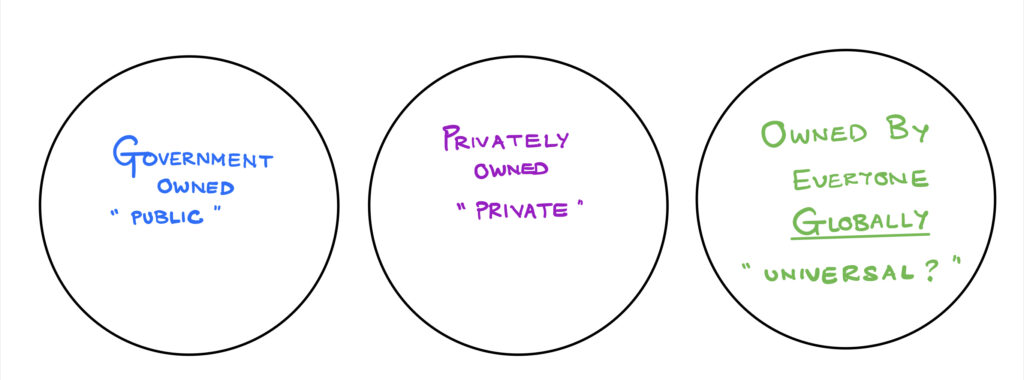

But governments don’t have terms to describe goods that are both non-gov’t and non-private, that are truly community owned.

I don’t know if there is a real world equivalent today for this. Even community-owned and operated parks are still on land that must be either public or private. Even a local cooperative is some sort of a private corporation. Joining such a cooperative requires permission from existing members.

The bitcoin and ethereum and numerous other blockchains are different because while they resemble cooperatives – community developed software running on private hardware powered by privately paid-for resources – it is permissionless. Anyone can run a full or light Bitcoin or Ethereum node, no permission/license required, and be a participant. Ditto with proof of stake blockchains. That is where the analogy with a community park breaks down, and that is what makes all the difference.

This is a new model, one we haven’t seen before. And this is why regulators and governments around the world still think of blockchains in terms of “if we don’t own it, we must regulate it”.

Back in July, Bitcoin had slumped to under half of its January highs of over $60,000. That dragged several other cryptocurrencies down with it, and the overall crypto market capitalisation fell several hundred billion dollars.Several friends and readers who held crypto messaged me asking whether they should get out and sell before the ‘market’ crashed further, or whether it was a good time and a good price to buy even more:

Like with any type of investing, if you aren’t clear about why you’re in it, the only thing you’re in for is anxiety. And that takes away from all the fun and fascination from the world of crypto.So I wrote a Twitter thread about it and shared it with all those friends. It’s helped a lot of them, so I’m posting it here with quick comments:

Some perspective on the extended #Bitcoin crash: BTC was below $30,000 yesterday. That’s well over 50% down from its all time high of nearly $65,000 in Apr ‘21.

The crash of 2017-18 was the meteor that wiped out the dinosaurs. It put an end to the scammy ICO era and allowed today’s incredible DeFi ecosystem to emerge.

However, #Bitcoin prices would not recover for another couple of years.

I’ve personally lost money in the June, September, November 2017 and the great December 2017 crash. The last one took nearly two years to recover from. But then it reached an all-time-high nearly three times its previous high. In that context, the recent July 2021 crash is nothing. Perspective is important.

Wondering what to buy or whether to buy at all? Think about why you got into crypto in the first place:

of it. Or you’re sure that the financial system is ripe for collapse, or are just seeing really cool projects being built on blockchains. It doesn’t matter how short-term, cynical, opportunistic your interest. Or how deep and well thought out your personal convictions are. As long as you’re aware of them.Having said that:

You believe in an alternative, government-free system of money? Buy BTC regardless. Buy monthly. You’re in it for the long term. The classic HODLer. Move it to a wallet whose keys you own.

You want to hedge your portfolio? What a great time to get into #Bitcoin. But: (1) cap it at the percentage that you’ve allocated to alternatives. And: (2) weigh the fact that bitcoin isn’t nearly as uncorrelated as it used to be. https://t.co/6057ItXCYM

You want to make a quick buck? Then your guess is as good as mine. But consider that the best gains are to be made in volatile times, so keep track of volatility. Now is probably a good time: pic.twitter.com/KYTlTZqE6T

As you read, if you can intuit and articulate your interest in the crypto space, you can craft a simple set of principles about when and what tokens to buy. I finished with this:

Do you know what the most interesting aspect of all this crazy rise and crash in 2021 is?

That #Bitcoin’s share of the over crypto market is the lowest it has ever been.

Not only is there a dizzying variety of tokens to evaluate, the value of many of those tokens now rivals Bitcoin and Ethereum. These latter two are far from the only influential projects in the crypto space any more. No matter what drives your interest in crypto, you have never had more choice to implement your investing plan than today.